What every older Canadian

shouldknow about

POWERS OF ATTORNEY

(for financial matters andproperty)

and

JOINT BANK

ACCOUNTS

FEDERAL/PROVINCIAL/TERRITORIAL MINISTERS RESPONSIBLE FOR SENIORS

LES MINISTRES FÉDÉRAL/PROVINCIAUX/TERRITORIAUX RESPONSABLES DES AÎNÉS

LES MINISTRES FÉDÉRAL/PROVINCIAUX/TERRITORIAUX RESPONSABLES DES AÎNÉS

FEDERAL/PROVINCIAL/TERRITORIAL MINISTERS RESPONSIBLE FOR SENIORS

FEDERAL/PROVINCIAL/TERRITORIAL MINISTERS RESPONSIBLE FOR SENIORS

LES MINISTRES FÉDÉRAL/PROVINCIAUX/TERRITORIAUX RESPONSABLES DES AÎNÉS

LES MINISTRES

FÉDÉRAL/PROVINCIAUX/TERRITORIAUX

RESPONSABLES DES AÎNÉS

FEDERAL/PROVINCIAL/TERRITORIAL

MINISTERS RESPONSIBLE FOR SENIORS

LES MINISTRES

FÉDÉRAL/PROVINCIAUX/TERRITORIAUX

RESPONSABLES DES AÎNÉS

FEDERAL/PROVINCIAL/TERRITORIAL

MINISTERS RESPONSIBLE FOR SENIORS

LES MINISTRES

FÉDÉRAL/PROVINCIAUX/TERRITORIAUX

RESPONSABLES DES AÎNÉS

FEDERAL/PROVINCIAL/TERRITORIAL

MINISTERS RESPONSIBLE FOR SENIORS

English/Français

Français/English

English

Français

English/Français

Français/English

Français

English

This document has been jointly prepared by the Forum

of Federal, Provincial and Territorial Ministers Responsible for

Seniors. The Forum is an intergovernmental body established

to share information, discuss new and emerging issues related

to seniors, and work collaboratively on key projects.

Québec’s participation in the development of this document

was aimed at sharing expertise, information and best practices.

However, Québec does not subscribe to, or take part in, an

integrated pan-Canadian approach in this eld and intends

to fully assume its responsibilities for seniors in Québec.

This document is available on demand in multiple formats

(large print, Braille, audio cassette, audio CD, e-text diskette,

e-text CD, or DAISY), by contacting 1 800 O-Canada

(1-800-622-6232). If you use a teletypewriter (TTY),

call 1-800-926-9105.

2013 All Rights Reserved

Paper

Cat. No.: HS4-118/2013

ISBN: 978-1-100-54410-6

PDF

Cat. No.: HS4-118/2013E-PDF

ISBN: 978-1-100-21223-4

Cat. No. : ISSD-106-09-13

This publication provides general information about

Powers of Attorney that deal with nances and property, and

general information about joint bank accounts.

When the term “Powers of Attorney” is used in this document,

it refers to Powers of Attorney for nances and property only.

This brochure does not deal with Powers of Attorney for

healthcare or personal care.

This publication is not a substitute for getting legal advice

for your own particular situation.

As laws dealing with Powers of Attorney are specic to each

province and territory, it is important to understand the laws

where you live before making any decisions.

It is also important, before opening a joint bank account,

to understand the legal consequences associated with such

accounts. Speak with your nancial institution about your wishes

so they can assist you with a nancial product that best suits

your needs.

Many Canadians are concerned about how to manage their

money, property, and nances as they age or as life changes take

place. They may worry about what will happen if they become

unable to deal with their own nances. It is a good idea to plan

ahead for a time when you may need help managing your affairs.

Two tools often used for managing nancial affairs are Powers

of Attorney and joint bank accounts.

It is important to know how a Power of Attorney or a joint bank

account works before you use them. There are risks and

advantages to both.

You should never feel pressured to sign a Power of Attorney or to

open a joint bank account. Carefully consider all of your options

before making any decisions.

1

Powers of Attorney

What is a Power of Attorney?

A Power of Attorney is a legal document that you sign to give one

person, or more than one person, the authority to manage your

money and property on your behalf. In most of Canada, the person

you appoint is called an “attorney.” That person does not need to

be a lawyer.

What types of Powers of Attorney are used in Canada?

The names and requirements for the different types of Powers of

Attorney that deal with nances and property will vary depending

on the province or territory where you live.

Among other requirements, you must be mentally capable at the

time you sign any type of Power of Attorney for it to be valid. In

general, to be mentally capable means that you are able to

understand and appreciate nancial and legal decisions and

understand the consequences of making these decisions.

However, the legal denition of mental capacity will vary based

on the laws in each province or territory.

Generally, there are two main types of Powers of Attorney

commonly used for nances and property in Canada:

A General Power of Attorney is a legal document that can give

your attorney authority over all or some of your nances and

property. It allows your attorney to manage your nances and

property on your behalf only while you are mentally capable of

managing your own affairs. It ends if you become mentally

incapable of managing your own affairs.

A general Power of Attorney can be ‘specic’ or ‘limited’, which

can give authority to your attorney for a limited task (e.g. sell a

house) or give them authority for a specic period of time. The

Power of Attorney can start as soon as you sign it, or it can start on

a specic date that you write in the document.

2

1

Powers of Attorney

What is a Power of Attorney?

A Power of Attorney is a legal document that you sign to give one

person, or more than one person, the authority to manage your

money and property on your behalf. In most of Canada, the person

you appoint is called an “attorney.” That person does not need to

be a lawyer.

What types of Powers of Attorney are used in Canada?

The names and requirements for the different types of Powers of

Attorney that deal with nances and property will vary depending

on the province or territory where you live.

Among other requirements, you must be mentally capable at the

time you sign any type of Power of Attorney for it to be valid. In

general, to be mentally capable means that you are able to

understand and appreciate nancial and legal decisions and

understand the consequences of making these decisions.

However, the legal denition of mental capacity will vary based

on the laws in each province or territory.

Generally, there are two main types of Powers of Attorney

commonly used for nances and property in Canada:

A General Power of Attorney is a legal document that can give

your attorney authority over all or some of your nances and

property. It allows your attorney to manage your nances and

property on your behalf only while you are mentally capable of

managing your own affairs. It ends if you become mentally

incapable of managing your own affairs.

A general Power of Attorney can be ‘specic’ or ‘limited’, which

can give authority to your attorney for a limited task (e.g. sell a

house) or give them authority for a specic period of time. The

Power of Attorney can start as soon as you sign it, or it can start on

a specic date that you write in the document.

1

Powers of Attorney

What is a Power of Attorney?

A Power of Attorney is a legal document that you sign to give one

person, or more than one person, the authority to manage your

money and property on your behalf. In most of Canada, the person

you appoint is called an “attorney.” That person does not need to

be a lawyer.

What types of Powers of Attorney are used in Canada?

The names and requirements for the different types of Powers of

Attorney that deal with nances and property will vary depending

on the province or territory where you live.

Among other requirements, you must be mentally capable at the

time you sign any type of Power of Attorney for it to be valid. In

general, to be mentally capable means that you are able to

understand and appreciate nancial and legal decisions and

understand the consequences of making these decisions.

However, the legal denition of mental capacity will vary based

on the laws in each province or territory.

Generally, there are two main types of Powers of Attorney

commonly used for nances and property in Canada:

A General Power of Attorney is a legal document that can give

your attorney authority over all or some of your nances and

property. It allows your attorney to manage your nances and

property on your behalf only while you are mentally capable of

managing your own affairs. It ends if you become mentally

incapable of managing your own affairs.

A general Power of Attorney can be ‘specic’ or ‘limited’, which

can give authority to your attorney for a limited task (e.g. sell a

house) or give them authority for a specic period of time. The

Power of Attorney can start as soon as you sign it, or it can start on

a specic date that you write in the document.

1

Powers of Attorney

What is a Power of Attorney?

A Power of Attorney is a legal document that you sign to give one

person, or more than one person, the authority to manage your

money and property on your behalf. In most of Canada, the person

you appoint is called an “attorney.” That person does not need to

be a lawyer.

What types of Powers of Attorney are used in Canada?

The names and requirements for the different types of Powers of

Attorney that deal with nances and property will vary depending

on the province or territory where you live.

Among other requirements, you must be mentally capable at the

time you sign any type of Power of Attorney for it to be valid. In

general, to be mentally capable means that you are able to

understand and appreciate nancial and legal decisions and

understand the consequences of making these decisions.

However, the legal denition of mental capacity will vary based

on the laws in each province or territory.

Generally, there are two main types of Powers of Attorney

commonly used for nances and property in Canada:

A General Power of Attorney is a legal document that can give

your attorney authority over all or some of your nances and

property. It allows your attorney to manage your nances and

property on your behalf only while you are mentally capable of

managing your own affairs. It ends if you become mentally

incapable of managing your own affairs.

A general Power of Attorney can be ‘specic’ or ‘limited’, which

can give authority to your attorney for a limited task (e.g. sell a

house) or give them authority for a specic period of time. The

Power of Attorney can start as soon as you sign it, or it can start on

a specic date that you write in the document.

1

Powers of Attorney

What is a Power of Attorney?

A Power of Attorney is a legal document that you sign to give one

person, or more than one person, the authority to manage your

money and property on your behalf. In most of Canada, the person

you appoint is called an “attorney.” That person does not need to

be a lawyer.

What types of Powers of Attorney are used in Canada?

The names and requirements for the different types of Powers of

Attorney that deal with nances and property will vary depending

on the province or territory where you live.

Among other requirements, you must be mentally capable at the

time you sign any type of Power of Attorney for it to be valid. In

general, to be mentally capable means that you are able to

understand and appreciate nancial and legal decisions and

understand the consequences of making these decisions.

However, the legal denition of mental capacity will vary based

on the laws in each province or territory.

Generally, there are two main types of Powers of Attorney

commonly used for nances and property in Canada:

A General Power of Attorney is a legal document that can give

your attorney authority over all or some of your nances and

property. It allows your attorney to manage your nances and

property on your behalf only while you are mentally capable of

managing your own affairs. It ends if you become mentally

incapable of managing your own affairs.

A general Power of Attorney can be ‘specic’ or ‘limited’, which

can give authority to your attorney for a limited task (e.g. sell a

house) or give them authority for a specic period of time. The

Power of Attorney can start as soon as you sign it, or it can start on

a specic date that you write in the document.

3

2

An Enduring or Continuing Power of Attorney is a legal document

that lets your attorney continue acting for you if you become

mentally incapable of managing your nances and property. It can

also give your attorney authority over all or some of your nances

and property. An Enduring or Continuing Power of Attorney can

take effect as soon as you sign it. In some cases, it is possible to

have the Power of Attorney come into effect only when you

become mentally incapable, if this was specied in the document.

What can my attorney do?

Unless you limit your attorney’s authority, they can do almost

everything with your nances and property that you could do. If

you don’t have any limitations in your Power of Attorney

document, your attorney can do your banking, sign cheques, buy

or sell real estate in your name, and buy consumer goods. Your

attorney does not become the owner of any of your money or

property. He or she only has the authority to manage it on your

behalf.

Your attorney cannot make a will for you, change your existing

will, change a beneciary on a life insurance plan, or give a new

Power of Attorney to someone else on your behalf.

Can my attorney make decisions about my healthcare

and personal care?

In most parts of Canada, it is possible to prepare documents that

give another person the authority to make health and other types

of personal and non-nancial decisions for you, if you were to

become mentally incapable of doing so for yourself. Depending

on where you live, these documents may be called Powers of

Attorney, personal or health directives, representation agreements,

or mandates.

These documents are not the same as Powers of Attorney for

nances and property. It is important to be clear about what type

of document you are signing. This publication deals with Powers of

Attorney for nancial matters and property only. This includes your

money, investments, and everything that you own, including your

home.

Can I still make decisions for myself if I grant someone

a Power of Attorney?

As long as you are mentally capable, you can continue to make

your own decisions about your nances.

Understand the laws where you live

Each province and territory has its own laws relating to Powers of

Attorney. You need to follow the law in the province or territory

where you live.

You may want to consult a lawyer when entering into a Power of

Attorney to be sure that your document is valid, and to fully

understand what your attorney will be able to do. It is important

that you learn how you or others can monitor your attorney’s

actions, and what to do if you want to change or cancel the Power

of Attorney. Be sure that you fully understand any document before

you sign it.

2

An Enduring or Continuing Power of Attorney is a legal document

that lets your attorney continue acting for you if you become

mentally incapable of managing your nances and property. It can

also give your attorney authority over all or some of your nances

and property. An Enduring or Continuing Power of Attorney can

take effect as soon as you sign it. In some cases, it is possible to

have the Power of Attorney come into effect only when you

become mentally incapable, if this was specied in the document.

What can my attorney do?

Unless you limit your attorney’s authority, they can do almost

everything with your nances and property that you could do. If

you don’t have any limitations in your Power of Attorney

document, your attorney can do your banking, sign cheques, buy

or sell real estate in your name, and buy consumer goods. Your

attorney does not become the owner of any of your money or

property. He or she only has the authority to manage it on your

behalf.

Your attorney cannot make a will for you, change your existing

will, change a beneciary on a life insurance plan, or give a new

Power of Attorney to someone else on your behalf.

Can my attorney make decisions about my healthcare

and personal care?

In most parts of Canada, it is possible to prepare documents that

give another person the authority to make health and other types

of personal and non-nancial decisions for you, if you were to

become mentally incapable of doing so for yourself. Depending

on where you live, these documents may be called Powers of

Attorney, personal or health directives, representation agreements,

or mandates.

These documents are not the same as Powers of Attorney for

nances and property. It is important to be clear about what type

of document you are signing. This publication deals with Powers of

Attorney for nancial matters and property only. This includes your

money, investments, and everything that you own, including your

home.

Can I still make decisions for myself if I grant someone

a Power of Attorney?

As long as you are mentally capable, you can continue to make

your own decisions about your nances.

Understand the laws where you live

Each province and territory has its own laws relating to Powers of

Attorney. You need to follow the law in the province or territory

where you live.

You may want to consult a lawyer when entering into a Power of

Attorney to be sure that your document is valid, and to fully

understand what your attorney will be able to do. It is important

that you learn how you or others can monitor your attorney’s

actions, and what to do if you want to change or cancel the Power

of Attorney. Be sure that you fully understand any document before

you sign it.

2

An Enduring or Continuing Power of Attorney is a legal document

that lets your attorney continue acting for you if you become

mentally incapable of managing your nances and property. It can

also give your attorney authority over all or some of your nances

and property. An Enduring or Continuing Power of Attorney can

take effect as soon as you sign it. In some cases, it is possible to

have the Power of Attorney come into effect only when you

become mentally incapable, if this was specied in the document.

What can my attorney do?

Unless you limit your attorney’s authority, they can do almost

everything with your nances and property that you could do. If

you don’t have any limitations in your Power of Attorney

document, your attorney can do your banking, sign cheques, buy

or sell real estate in your name, and buy consumer goods. Your

attorney does not become the owner of any of your money or

property. He or she only has the authority to manage it on your

behalf.

Your attorney cannot make a will for you, change your existing

will, change a beneciary on a life insurance plan, or give a new

Power of Attorney to someone else on your behalf.

Can my attorney make decisions about my healthcare

and personal care?

In most parts of Canada, it is possible to prepare documents that

give another person the authority to make health and other types

of personal and non-nancial decisions for you, if you were to

become mentally incapable of doing so for yourself. Depending

on where you live, these documents may be called Powers of

Attorney, personal or health directives, representation agreements,

or mandates.

These documents are not the same as Powers of Attorney for

nances and property. It is important to be clear about what type

of document you are signing. This publication deals with Powers of

Attorney for nancial matters and property only. This includes your

money, investments, and everything that you own, including your

home.

Can I still make decisions for myself if I grant someone

a Power of Attorney?

As long as you are mentally capable, you can continue to make

your own decisions about your nances.

Understand the laws where you live

Each province and territory has its own laws relating to Powers of

Attorney. You need to follow the law in the province or territory

where you live.

You may want to consult a lawyer when entering into a Power of

Attorney to be sure that your document is valid, and to fully

understand what your attorney will be able to do. It is important

that you learn how you or others can monitor your attorney’s

actions, and what to do if you want to change or cancel the Power

of Attorney. Be sure that you fully understand any document before

you sign it.

4

3

These documents are not the same as Powers of Attorney for

nances and property. It is important to be clear about what type

of document you are signing. This publication deals with Powers of

Attorney for nancial matters and property only. This includes your

money, investments, and everything that you own, including your

home.

Can I still make decisions for myself if I grant someone

a Power of Attorney?

As long as you are mentally capable, you can continue to make

your own decisions about your nances.

Understand the laws where you live

Each province and territory has its own laws relating to Powers of

Attorney. You need to follow the law in the province or territory

where you live.

You may want to consult a lawyer when entering into a Power of

Attorney to be sure that your document is valid, and to fully

understand what your attorney will be able to do. It is important

that you learn how you or others can monitor your attorney’s

actions, and what to do if you want to change or cancel the Power

of Attorney. Be sure that you fully understand any document before

you sign it.

3

These documents are not the same as Powers of Attorney for

nances and property. It is important to be clear about what type

of document you are signing. This publication deals with Powers of

Attorney for nancial matters and property only. This includes your

money, investments, and everything that you own, including your

home.

Can I still make decisions for myself if I grant someone

a Power of Attorney?

As long as you are mentally capable, you can continue to make

your own decisions about your nances.

Understand the laws where you live

Each province and territory has its own laws relating to Powers of

Attorney. You need to follow the law in the province or territory

where you live.

You may want to consult a lawyer when entering into a Power of

Attorney to be sure that your document is valid, and to fully

understand what your attorney will be able to do. It is important

that you learn how you or others can monitor your attorney’s

actions, and what to do if you want to change or cancel the Power

of Attorney. Be sure that you fully understand any document before

you sign it.

5

4

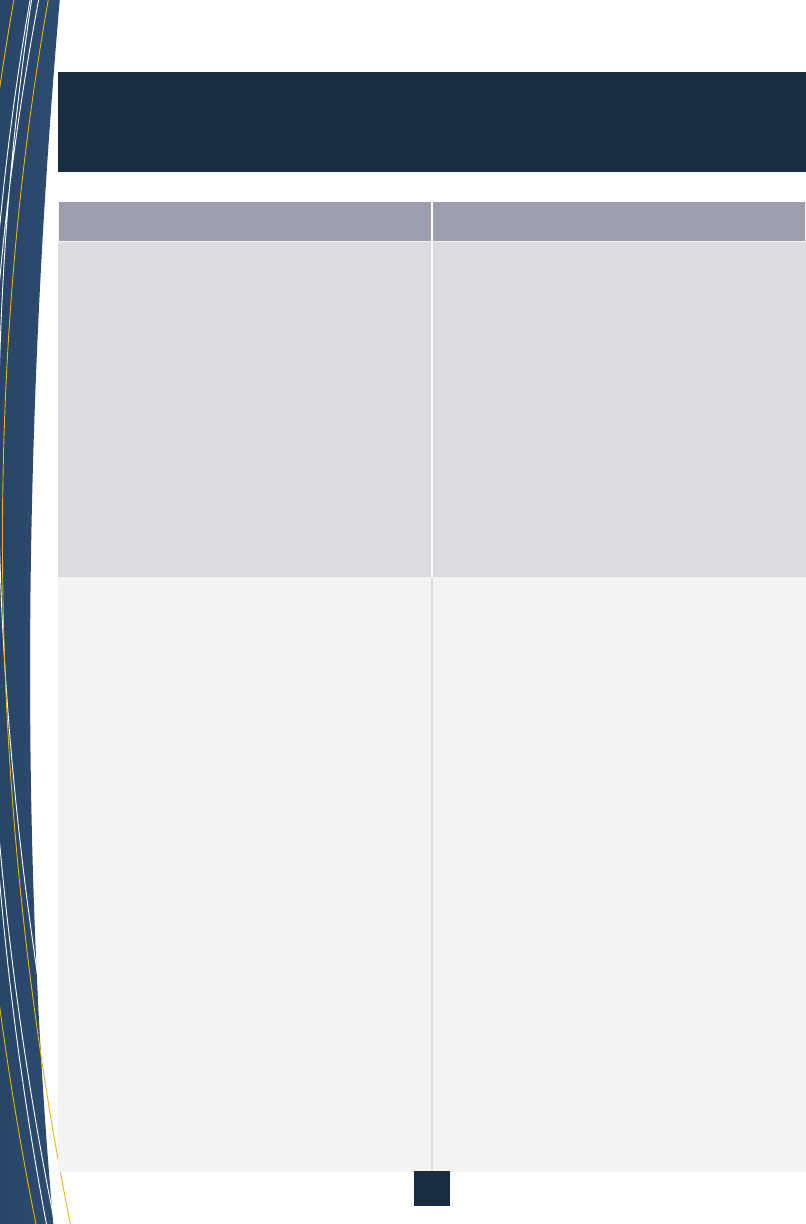

What are the advantages and risks of having

a Power of Attorney?

Advantages Risks

Practical

• Makes it clear who will be

responsible for your money and

property if you can’t manage

them on your own, even

temporarily.

• Your attorney must manage your

money and property for your

benet and can be required by

law to account for and explain

how he or she is managing it.

May make you vulnerable to

nancial abuse

• Can lead to mismanagement of

your money and property if the

attorney you choose is not

trustworthy, uses your money

improperly, or does not make

decisions that are in your best

interest.

Flexible

• Can be as general or specic as

you need.

• You can choose to appoint two or

more attorneys. You can require

that your attorneys make all

decisions together (“jointly”),

or to act together or separately,

if one of them is unavailable

(“jointly and severally”). You can

also appoint alternate or

successive attorneys.

• Having two or more attorneys

could reduce potential fraudulent

use of a Power of Attorney.

Too directive or not specic

enough

• Not enough information or

limitations in the document could

lead to the mismanagement of

your nances or to your nances

being managed in a way that you

do not agree with.

• Your attorney must manage your

affairs in the way that you direct

in the document. Strict limitations

can make it difcult for your

attorney to take care of your

nances.

• If you appoint more than one

attorney to act jointly,

disagreements between them

could cause problems and lead to

delays in the management of your

nancial affairs.

Convenient

• A general Power of Attorney

allows your attorney to look after

your affairs if you are away

temporarily or if you need help

managing your affairs.

• An Enduring Power of Attorney

allows your attorney to continue

looking after your affairs if you

lose your mental capacity.

• If you lose your mental capacity

and do not have a valid Power of

Attorney document in place,

someone will need to get

authority from the court to

manage your money and property.

This can be time consuming and

expensive.

Not up-to-date

• If not reviewed regularly, your

Power of Attorney document

might not meet your current needs

or the requirements of the law.

• The person you previously

selected to be your attorney may

no longer be the best choice or

may no longer be available.

• Possibility of ‘competing’ Powers

of Attorney if you have signed

more than one Power of Attorney

document. If you appoint a new

attorney, you should cancel your

previous Power of Attorney

document and advise your

nancial institution of the change.

Risks

6

5

What are the advantages and risks of having

a Power of Attorney?

Advantages Risks

Practical

• Makes it clear who will be

responsible for your money and

property if you can’t manage

them on your own, even

temporarily.

• Your attorney must manage your

money and property for your

benet and can be required by

law to account for and explain

how he or she is managing it.

May make you vulnerable to

nancial abuse

• Can lead to mismanagement of

your money and property if the

attorney you choose is not

trustworthy, uses your money

improperly, or does not make

decisions that are in your best

interest.

Flexible

• Can be as general or specic as

you need.

• You can choose to appoint two or

more attorneys. You can require

that your attorneys make all

decisions together (“jointly”),

or to act together or separately,

if one of them is unavailable

(“jointly and severally”). You can

also appoint alternate or

successive attorneys.

• Having two or more attorneys

could reduce potential fraudulent

use of a Power of Attorney.

Convenient

• A general Power of Attorney

allows your attorney to look after

your affairs if you are away

temporarily or if you need help

managing your affairs.

• An Enduring Power of Attorney

allows your attorney to continue

looking after your affairs if you

lose your mental capacity.

• If you lose your mental capacity

and do not have a valid Power of

Attorney document in place,

someone will need to get

authority from the court to

manage your money and property.

This can be time consuming and

expensive.

Not up-to-date

• If not reviewed regularly, your

Power of Attorney document

might not meet your current needs

or the requirements of the law.

• The person you previously

selected to be your attorney may

no longer be the best choice or

may no longer be available.

• Possibility of ‘competing’ Powers

of Attorney if you have signed

more than one Power of Attorney

document. If you appoint a new

attorney, you should cancel your

previous Power of Attorney

document and advise your

nancial institution of the change.

Advantages Risks

7

6

Choosing an attorney

Who can I ask to be my attorney?

You should ask someone you trust. You may choose your spouse, a

close friend, a family member or anyone else that you trust.

Carefully consider whether they are the best choice to manage

your money and property, and do so in your best interest.

The minimum legal age for an attorney varies according to the

province or territory where you live. The person you ask to be your

attorney can refuse to act for you, so it is important to ask the

person rst if they are willing to take on this responsibility and

everything that it entails. You should also consider appointing a

substitute attorney in case the rst attorney can no longer act for

you.

Do I have to pay my attorney?

In some provinces, unless you state otherwise in the Power of

Attorney, a person appointed under a continuing Power of Attorney

may have a right to be paid. Before you sign any documents, it is a

good idea to have a conversation with the person you choose as

your attorney regarding compensation for their work. You should

include this information in your Power of Attorney document.

You may also consider appointing a trust company or a legal or

nancial professional with the skills to manage nances and

property. You will probably need to pay fees for this service. Also,

these options may only be available to you if your property is over

a certain value.

What are my attorney’s legal responsibilities?

The attorney’s role carries many legal responsibilities. Your attorney

must comply with the legal duties and responsibilities of attorneys

in the province or territory where you live. Your attorney must

manage your nances and property, and keep records, according

to any directions you have given in your Power of Attorney

document. They must act in your best interest. However, there is

always a risk that they may not do so, which is why it is important

to name someone that you can really trust and that understands

the legal responsibilities they will be taking on.

8

7

Choosing an attorney

Who can I ask to be my attorney?

You should ask someone you trust. You may choose your spouse, a

close friend, a family member or anyone else that you trust.

Carefully consider whether they are the best choice to manage

your money and property, and do so in your best interest.

The minimum legal age for an attorney varies according to the

province or territory where you live. The person you ask to be your

attorney can refuse to act for you, so it is important to ask the

person rst if they are willing to take on this responsibility and

everything that it entails. You should also consider appointing a

substitute attorney in case the rst attorney can no longer act for

you.

Do I have to pay my attorney?

In some provinces, unless you state otherwise in the Power of

Attorney, a person appointed under a continuing Power of Attorney

may have a right to be paid. Before you sign any documents, it is a

good idea to have a conversation with the person you choose as

your attorney regarding compensation for their work. You should

include this information in your Power of Attorney document.

You may also consider appointing a trust company or a legal or

nancial professional with the skills to manage nances and

property. You will probably need to pay fees for this service. Also,

these options may only be available to you if your property is over

a certain value.

What are my attorney’s legal responsibilities?

The attorney’s role carries many legal responsibilities. Your attorney

must comply with the legal duties and responsibilities of attorneys

in the province or territory where you live. Your attorney must

manage your nances and property, and keep records, according

to any directions you have given in your Power of Attorney

document. They must act in your best interest. However, there is

always a risk that they may not do so, which is why it is important

to name someone that you can really trust and that understands

the legal responsibilities they will be taking on.

9

8

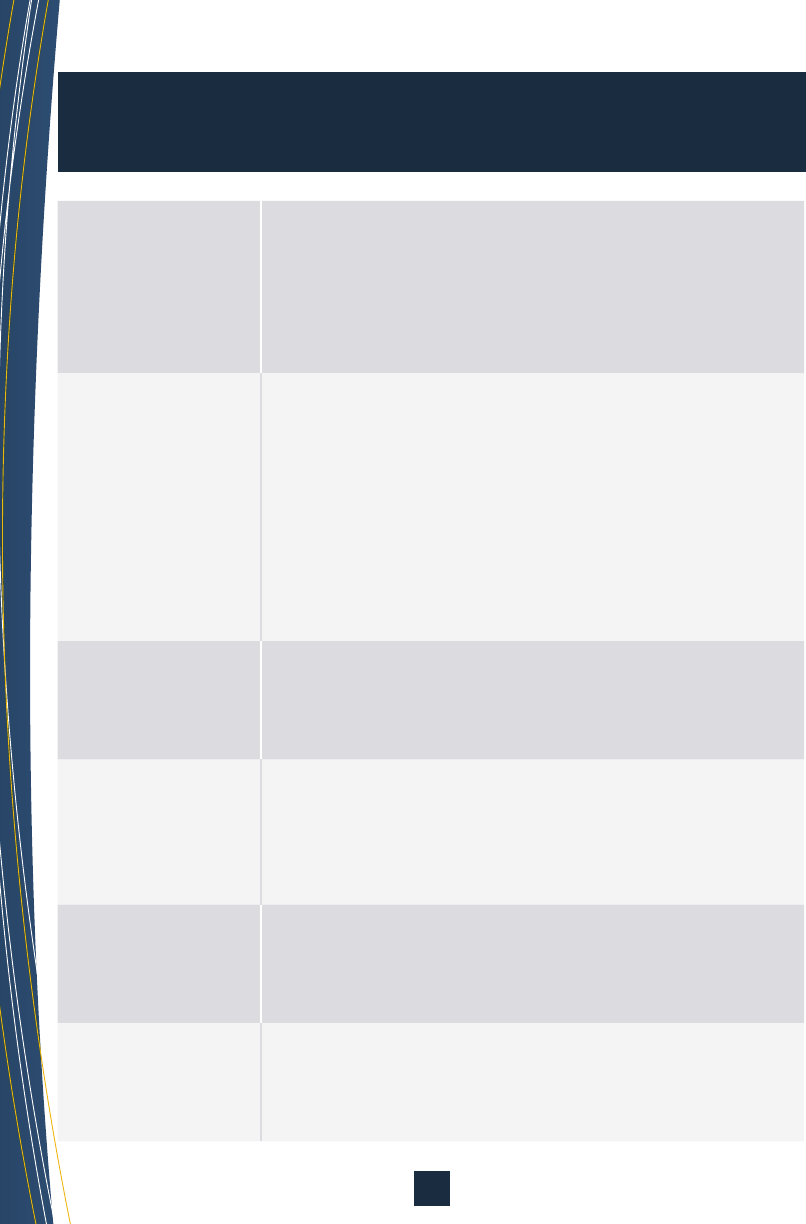

What to consider when choosing an attorney

Personal

Suitability

• Does this person know how to manage money and

property? Do they do it well for themselves?

• Do you think this person will manage your money

and property in the way that you want and in your

best interest?

Trustworthiness

• Has this person always been open and honest with

you?

• Have you known this person long enough or well

enough to feel that you can trust them?

• Is this person able to act in your best interest?

Do they have any personal issues (e.g. nancial

problems or health concerns) that may interfere

with them properly managing your nances?

Experience

• Does this person understand nancial matters?

• Does this person understand the duties and

responsibilities involved in being your attorney?

Availability

• Does the person have the time to handle your

money and property as well as their own?

• Does this person live nearby and is he or she easy

to contact and readily available?

Reliability

• Has this person been someone you could rely on?

• Has this person carried through on important

decisions or duties in the past?

Willingness

• Has this person agreed to take on the responsibility?

• Does this person clearly understand what is expected

of them as your attorney?

What to consider BEFORE preparing a Power of Attorney

• Understand how the different types of Powers of Attorney work, and

decide what type will best suit your needs.

• Decide when you want the Power of Attorney to start.

• Find out how the Power of Attorney can come to an end, how you can

cancel or change the Power of Attorney, and what happens if you or

your attorney were to lose mental capacity or pass away. These answers

may vary depending on where you live.

• Make sure the person you choose is someone that you can trust to

manage your money and property in the way that you want.

• Make sure your attorney understands, or is willing to learn, his or her

legal responsibilities and duties.

• Decide whether you want to give your attorney authority over some or

all of your nancial matters (including bank accounts), and whether it

will be for general or specic purposes.

• Decide whether you want regular updates (e.g. account statements)

from your attorney sent to you, or a person you name, to check that

your affairs are being properly managed.

• If you use a Power of Attorney kit or forms from a website to set up

your Power of Attorney, you need to be sure the form is signed in

compliance with the law in your province or territory.

• Consider having a lawyer review the document to make sure that it is valid.

• Decide whether you want to appoint one or more persons, and whether

they can act alone or must act together.

• If you appoint more than one attorney, and they must act together,

consider appointing a third person or including a mechanism to resolve

disputes if the attorneys can’t agree.

• Consider appointing a substitute attorney in case your attorney is

no longer able to act for you.

10

9

What to consider when choosing an attorney

Personal

Suitability

• Does this person know how to manage money and

property? Do they do it well for themselves?

• Do you think this person will manage your money

and property in the way that you want and in your

best interest?

Trustworthiness

• Has this person always been open and honest with

you?

• Have you known this person long enough or well

enough to feel that you can trust them?

• Is this person able to act in your best interest?

Do they have any personal issues (e.g. nancial

problems or health concerns) that may interfere

with them properly managing your nances?

Experience

• Does this person understand nancial matters?

• Does this person understand the duties and

responsibilities involved in being your attorney?

Availability

• Does the person have the time to handle your

money and property as well as their own?

• Does this person live nearby and is he or she easy

to contact and readily available?

Reliability

• Has this person been someone you could rely on?

• Has this person carried through on important

decisions or duties in the past?

Willingness

• Has this person agreed to take on the responsibility?

• Does this person clearly understand what is expected

of them as your attorney?

What to consider BEFORE preparing a Power of Attorney

• Understand how the different types of Powers of Attorney work, and

decide what type will best suit your needs.

• Decide when you want the Power of Attorney to start.

• Find out how the Power of Attorney can come to an end, how you can

cancel or change the Power of Attorney, and what happens if you or

your attorney were to lose mental capacity or pass away. These answers

may vary depending on where you live.

• Make sure the person you choose is someone that you can trust to

manage your money and property in the way that you want.

• Make sure your attorney understands, or is willing to learn, his or her

legal responsibilities and duties.

• Decide whether you want to give your attorney authority over some or

all of your nancial matters (including bank accounts), and whether it

will be for general or specic purposes.

• Decide whether you want regular updates (e.g. account statements)

from your attorney sent to you, or a person you name, to check that

your affairs are being properly managed.

• If you use a Power of Attorney kit or forms from a website to set up

your Power of Attorney, you need to be sure the form is signed in

compliance with the law in your province or territory.

• Consider having a lawyer review the document to make sure that it is valid.

• Decide whether you want to appoint one or more persons, and whether

they can act alone or must act together.

• If you appoint more than one attorney, and they must act together,

consider appointing a third person or including a mechanism to resolve

disputes if the attorneys can’t agree.

• Consider appointing a substitute attorney in case your attorney is

no longer able to act for you.

11

10

What to consider AFTER you prepared a Power of Attorney

• Review the terms of your Power of Attorney regularly to make sure

it is still valid and still reects how you want your money and property

managed.

• You can make changes to your Power of Attorney, cancel your Power

of Attorney, change your attorney, or name more than one attorney,

at any time, as long as you are mentally capable. If you make any

changes, you should advise your nancial institution immediately.

• Continue to review your own nancial records on a regular basis

for as long as you can.

• Assigning a Power of Attorney does not prevent you from continuing to

manage some or all of your affairs, as long as you are mentally capable.

• Talk to your attorney regularly so that you can understand how they are

handling your money and property.

• Even though your attorney is taking care of things for you, you always

have the right to ask questions and get answers from them about your

money and property.

• If you have questions or concerns about how your attorney is managing

your affairs, you can speak to someone at your nancial institution

or seek legal advice. Attorneys can be held responsible if they fail to

manage affairs as directed in a Power of Attorney document.

• Understand that signing a new Power of Attorney, including one signed

at a bank, may cancel the previous one that you had signed.

• If you move or will need to use the Power of Attorney in another province,

territory, or country, get legal advice to be sure the document will be

recognized. It may be necessary for you to make a new document for

certain assets.

What if my bank wants me to sign

a Power of Attorney form?

Banks, credit unions and other nancial institutions may also have

their own forms to appoint an attorney to make decisions about a

specic account or property that you have with that institution.

If you already have your own Power of Attorney that gives your

attorney authority over all of your nancial affairs, including

accounts with that nancial institution, it likely isn’t necessary for

you to sign the bank’s form.

Before you decide whether or not you want to sign the bank’s

form, you may want to review it with your lawyer or with another

person whose opinion you trust. You can also show your own

Power of Attorney to the bank manager or a knowledgeable bank

representative and ask them to conrm that it can be used for

banking purposes. If you sign the bank’s form, there is a possibility

that your other Power of Attorney could become invalid.

12

11

What if my bank wants me to sign

a Power of Attorney form?

Banks, credit unions and other nancial institutions may also have

their own forms to appoint an attorney to make decisions about a

specic account or property that you have with that institution.

If you already have your own Power of Attorney that gives your

attorney authority over all of your nancial affairs, including

accounts with that nancial institution, it likely isn’t necessary for

you to sign the bank’s form.

Before you decide whether or not you want to sign the bank’s

form, you may want to review it with your lawyer or with another

person whose opinion you trust. You can also show your own

Power of Attorney to the bank manager or a knowledgeable bank

representative and ask them to conrm that it can be used for

banking purposes. If you sign the bank’s form, there is a possibility

that your other Power of Attorney could become invalid.

13

12

Joint Bank Accounts

Financial institutions such as banks, credit unions and trust

companies may offer customers the option to set up a joint

account. When the phrase “joint bank account” or “joint account”

is used in this brochure it refers to joint accounts at any of these

nancial institutions.

What is a joint bank account?

Joint accounts are bank accounts in which two or more people

have ownership rights over the same account. These rights include

the right for all account holders to deposit, withdraw, or deal with

the funds in the account, no matter who puts the money into

the account.

How does a joint account work?

As a joint account holder, you share equal access to the account

and responsibility for all the transactions made through

the account. In most cases, unless you state otherwise, the other

account holder can make transactions without your consent.

In some cases, it may be possible to specify that the consent of all

joint account holders is required to access the funds in the

account.

In many cases, joint accounts include the right of survivorship.

This means that if one of the account holders dies, the surviving

account holder becomes the owner of the account, with the right

to deposit, withdraw, and deal with the funds in the account.

However, in some cases this could be challenged by others who

may think they have an interest in the money in the account as an

inheritance. The surviving joint account holder may have to

demonstrate that the deceased account holder intended the

remaining funds be a gift to the joint account holder. This could

potentially lead to delays in the surviving account holder being

able to access funds in the account.

Note: In Québec, a joint account is frozen upon the death

of one of the joint account holders. Consult with your banking

institution to obtain more specic information about how

this works.

Ask questions

Find out how joint accounts work at your nancial institution and

ask about what happens if a joint account holder dies. Make sure

you fully understand all this information before making

any decisions.

14

13

Joint Bank Accounts

Financial institutions such as banks, credit unions and trust

companies may offer customers the option to set up a joint

account. When the phrase “joint bank account” or “joint account”

is used in this brochure it refers to joint accounts at any of these

nancial institutions.

What is a joint bank account?

Joint accounts are bank accounts in which two or more people

have ownership rights over the same account. These rights include

the right for all account holders to deposit, withdraw, or deal with

the funds in the account, no matter who puts the money into

the account.

How does a joint account work?

As a joint account holder, you share equal access to the account

and responsibility for all the transactions made through

the account. In most cases, unless you state otherwise, the other

account holder can make transactions without your consent.

In some cases, it may be possible to specify that the consent of all

joint account holders is required to access the funds in the

account.

In many cases, joint accounts include the right of survivorship.

This means that if one of the account holders dies, the surviving

account holder becomes the owner of the account, with the right

to deposit, withdraw, and deal with the funds in the account.

However, in some cases this could be challenged by others who

may think they have an interest in the money in the account as an

inheritance. The surviving joint account holder may have to

demonstrate that the deceased account holder intended the

remaining funds be a gift to the joint account holder. This could

potentially lead to delays in the surviving account holder being

able to access funds in the account.

Note: In Québec, a joint account is frozen upon the death

of one of the joint account holders. Consult with your banking

institution to obtain more specic information about how

this works.

Ask questions

Find out how joint accounts work at your nancial institution and

ask about what happens if a joint account holder dies. Make sure

you fully understand all this information before making

any decisions.

15

14

Why set up a joint bank account?

There are many reasons why someone may consider opening a

joint account. For example, couples may set up a joint account to

pay household bills or deal with other shared expenses. This is one

of the most common uses of joint accounts.

In some cases, joint accounts may be considered as an option for

someone to get help from family members or friends to pay bills

and manage their nances.

For example, health conditions or mobility issues could make it

difcult for someone to manage their personal banking on their

own. Getting to the bank or using online banking services can be

difcult for some people. A person may consider setting up a joint

account with a family member, such as an adult child, after the

death of a spouse who used to deal with the household nances.

It may also be important to consider other consequences of a joint

account such as whether probate fees or taxes will apply upon the

death of a joint account holder or whether the remaining funds are

intended to form part of the deceased’s estate or be gifted to the

surviving joint account holder. These considerations may be

addressed in consultation with a lawyer.

16

15

Why set up a joint bank account?

There are many reasons why someone may consider opening a

joint account. For example, couples may set up a joint account to

pay household bills or deal with other shared expenses. This is one

of the most common uses of joint accounts.

In some cases, joint accounts may be considered as an option for

someone to get help from family members or friends to pay bills

and manage their nances.

For example, health conditions or mobility issues could make it

difcult for someone to manage their personal banking on their

own. Getting to the bank or using online banking services can be

difcult for some people. A person may consider setting up a joint

account with a family member, such as an adult child, after the

death of a spouse who used to deal with the household nances.

It may also be important to consider other consequences of a joint

account such as whether probate fees or taxes will apply upon the

death of a joint account holder or whether the remaining funds are

intended to form part of the deceased’s estate or be gifted to the

surviving joint account holder. These considerations may be

addressed in consultation with a lawyer.

Risks of a Joint Account

Control over the joint account

• Unless you are able to state otherwise in your banking agreement,

any person named on the joint account is able to withdraw money from

the account at any time. They don’t need permission from you to do so,

even if most or all the funds in the account were deposited by you.

• Funds withdrawn may never be recovered.

Relationship breakdown

• If the relationship between you and your joint account holder breaks

down, you risk the money being withdrawn or that the account may not

be handled in the way that you wished.

• If your joint account holder and their spouse separate or divorce,

the money in the joint account could be claimed in the separation or

divorce settlement.

Accountability

• It is difcult to hold a joint account holder legally accountable

for taking money from the account that they weren’t supposed to.

• You may have to go to court to challenge the actions of a joint account

holder. This could be expensive and stressful. It may also take a long

time to resolve.

Legal disputes

• If it is not clear that the money in the account was meant to be a gift to

the surviving joint account holder or whether it was meant to become

part of the deceased joint account holder’s estate, legal disputes could

arise.

• Legal disputes can be expensive and difcult to resolve.

17

16

Creditors

• You will share responsibility with your joint holder for all transactions

made through the account.

• If one of the joint account holders has nancial problems or declares

bankruptcy, creditors could make claims on the money in the account.

Removing someone from a joint account

• The bank may require both people named in the joint account to give

approval to remove one of you from the account.

What to consider before setting up

a joint bank account

Discuss the risks and

benets of a joint

account with people

you trust

• Do you understand how a joint account works?

• Do you understand that your joint account holder

will have equal ownership of the account with

you? This means they will have the right to

withdraw and use the money in the account even

if you deposited all the money.

Meet with a nancial

advisor to nd the

right banking options

for your needs

• Have you met with a nancial advisor to discuss

different types of accounts, and what will work

best for you?

• If you are having difculty with in-person

banking, have you considered pre-authorized

deposits and bill payments from your own

account, instead of opening a joint account?

Is the person you

want to name as joint

account holder

trustworthy?

• Has this person always been open and honest

with you?

• Have you known this person long enough or

well enough to feel that you can trust them?

• Is this person able to act in your best interest?

Do they have any personal issues that may

interfere with them properly managing your

nances?

18

17

Creditors

• You will share responsibility with your joint holder for all transactions

made through the account.

• If one of the joint account holders has nancial problems or declares

bankruptcy, creditors could make claims on the money in the account.

Removing someone from a joint account

• The bank may require both people named in the joint account to give

approval to remove one of you from the account.

What to consider before setting up

a joint bank account

Discuss the risks and

benets of a joint

account with people

you trust

• Do you understand how a joint account works?

• Do you understand that your joint account holder

will have equal ownership of the account with

you? This means they will have the right to

withdraw and use the money in the account even

if you deposited all the money.

Meet with a nancial

advisor to nd the

right banking options

for your needs

• Have you met with a nancial advisor to discuss

different types of accounts, and what will work

best for you?

• If you are having difculty with in-person

banking, have you considered pre-authorized

deposits and bill payments from your own

account, instead of opening a joint account?

Is the person you

want to name as joint

account holder

trustworthy?

• Has this person always been open and honest

with you?

• Have you known this person long enough or

well enough to feel that you can trust them?

• Is this person able to act in your best interest?

Do they have any personal issues that may

interfere with them properly managing your

nances?

19

18

How much control

will you have over

the money in

the account?

• Have you discussed with your nancial

institution if there are ways to keep some control

over withdrawals from the account?

• Are you able to put any restrictions on the

account (e.g. putting restrictions on cheques

written from the account)?

• Have you considered setting up online banking

alerts to be notied when there are withdrawals

or other activity on the joint account?

• Are you able to check the account statements

regularly?

What if something

happens to one of

the account holders?

• Speak to someone at your nancial institution or

a lawyer to nd out what happens if you or your

joint account holder dies or if one of the

account holders loses mental capacity.

• Consider including information about your joint

account in your will, so that your wishes are

clear.

Consider all your options

Even though setting up a joint bank account may seem to be a

convenient option to get help managing your nances, there are many

risks involved. Carefully consider all the risks and get information

about all the options available to you before making any decisions.

If you prepare a detailed Power of Attorney that gives your attorney

the authority to access specic bank accounts, they will be able to

help you pay your bills and manage your nances.

With a Power of Attorney document, you can limit what your attorney

is allowed to do. With a joint bank account, you may not be able to

limit what your joint account holder can do with the money in the

account.

There are also mechanisms in place to hold an attorney accountable

if they mismanage your nances or do not manage your money in the

way that you directed them to in the Power of Attorney document. It

is very difcult to hold a joint bank account holder accountable for

the mismanagement of money in the account.

Where can I nd more information?

For more information on Powers of Attorney and joint bank accounts,

contact knowledgeable professionals in your community, including

legal aid services or associations that offer public legal education and

information. You may also want to speak with a lawyer, an estate

planner, or someone knowledgeable at your bank, credit union or trust

company.

Powers of Attorney and joint bank accounts are not the only nancial

planning tools available. If you become incapable of managing your

own nances and property, and you do not have a Power of Attorney

or joint bank account, each province and territory has laws that allow

someone else to get legal authority to manage your nances for you.

For information on other seniors-related issues, visit seniors.gc.ca, your

local Service Canada ofce, or contact your provincial or territorial

government.

20

19

How much control

will you have over

the money in

the account?

• Have you discussed with your nancial

institution if there are ways to keep some control

over withdrawals from the account?

• Are you able to put any restrictions on the

account (e.g. putting restrictions on cheques

written from the account)?

• Have you considered setting up online banking

alerts to be notied when there are withdrawals

or other activity on the joint account?

• Are you able to check the account statements

regularly?

What if something

happens to one of

the account holders?

• Speak to someone at your nancial institution or

a lawyer to nd out what happens if you or your

joint account holder dies or if one of the

account holders loses mental capacity.

• Consider including information about your joint

account in your will, so that your wishes are

clear.

Consider all your options

Even though setting up a joint bank account may seem to be a

convenient option to get help managing your nances, there are many

risks involved. Carefully consider all the risks and get information

about all the options available to you before making any decisions.

If you prepare a detailed Power of Attorney that gives your attorney

the authority to access specic bank accounts, they will be able to

help you pay your bills and manage your nances.

With a Power of Attorney document, you can limit what your attorney

is allowed to do. With a joint bank account, you may not be able to

limit what your joint account holder can do with the money in the

account.

There are also mechanisms in place to hold an attorney accountable

if they mismanage your nances or do not manage your money in the

way that you directed them to in the Power of Attorney document. It

is very difcult to hold a joint bank account holder accountable for

the mismanagement of money in the account.

Where can I nd more information?

For more information on Powers of Attorney and joint bank accounts,

contact knowledgeable professionals in your community, including

legal aid services or associations that offer public legal education and

information. You may also want to speak with a lawyer, an estate

planner, or someone knowledgeable at your bank, credit union or trust

company.

Powers of Attorney and joint bank accounts are not the only nancial

planning tools available. If you become incapable of managing your

own nances and property, and you do not have a Power of Attorney

or joint bank account, each province and territory has laws that allow

someone else to get legal authority to manage your nances for you.

For information on other seniors-related issues, visit seniors.gc.ca, your

local Service Canada ofce, or contact your provincial or territorial

government.

21