February 2022

Mandatory climate-related

financial disclosures by

publicly quoted companies,

large private companies and

LLPs

Non-binding guidance

© Crown copyright 2022

This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated.

To view this licence, visit nationalarchives.gov.uk/doc/open-government-licence/version/3

or write to the

Information Policy Team, The National Archives, Kew, London TW9 4DU, or email:

psi@nationalarchives.gsi.gov.uk.

Where we have identified any third-party copyright information you will need to obtain permission from the

copyright holders concerned.

Any enquiries regarding this publication should be sent to us at:

climatedisclosure@beis.gov.uk

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

3

Contents

Section 1 _________________________________________________________________ 4

A. Introduction ___________________________________________________________ 4

B. Overview of the new climate-related financial disclosure requirements ______________ 5

C. Scope ________________________________________________________________ 7

D. Timing _______________________________________________________________ 9

E. Reporting requirements under sections 414CA and 414CB of the Companies Act 2006

and Regulations 12A and 12B of the Limited Liability Partnerships (Accounts and Audit)

(Application of Companies Act 2006) Regulations 2008. ___________________________ 9

Section 2 ________________________________________________________________ 19

A. Interaction with other regulation and frameworks ______________________________ 19

B. Links to additional information ____________________________________________ 21

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

4

Section 1

A. Introduction

The purpose of this document is to help companies and limited liability partnerships (LLPs)

understand how to meet new mandatory climate-related financial disclosure requirements

under the Companies (Strategic Report) (Climate-related Financial Disclosure) Regulations

2022

1

and the Limited Liability Partnerships (Climate-related Financial Disclosure) Regulations

2022

2

. These were made on 17

th

January 2022 and apply to reporting for financial years

starting on or after 6

th

April 2022.

This document is intended as a factual explanation of the secondary legislation. It is not

intended to be exhaustive, and companies and LLPs should not rely on it for legal guidance on

how the requirements will affect them. The guidance is published by the Secretary of State for

the Department of Business, Energy and Industrial Strategy in exercise of the powers granted

to him by the regulations.

The Department welcomes feedback on this document, particularly from business users who

are preparing or interpreting disclosures required under the regulations. Please send any

comments to climatedisclosure@beis.gov.uk.

This guidance will be reviewed periodically and updated where necessary.

1

https://www.legislation.gov.uk/uksi/2022/31/made

2

https://www.legislation.gov.uk/uksi/2022/46/contents/made

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

5

B. Overview of the new climate-related financial disclosure

requirements

Climate change poses risks to companies, financial institutions and individuals alike.

Both physical and transition risks could have material impacts on the value of companies and

their assets. Physical risks are those arising from the climatic impact of higher average

temperatures (such as the increased frequency and severity of extreme weather events), whilst

transition risks are those arising from the changes in technology, markets, policy, regulation,

and consumer sentiment which will result from our transition to net zero.

Disclosures of material climate-related financial information can help support investment

decisions as we move towards a low-carbon economy. As it becomes easier to compare

companies’ exposures to climate-related risks and opportunities, investors will be better

equipped to incorporate these risks into their investment and business decisions, and this also

provides greater information to other stakeholders for relevant decisions. The preparation by

businesses of disclosures on what the changing climate will mean for them, its impacts, risks,

and opportunities, may help them gauge what they need to do to address these for their

organisation, operations, and people.

The government recognises the recommendations of the Financial Stability Board’s (FSB)

Task Force on Climate-related Financial Disclosures (TCFD) as one of the most effective

frameworks for companies to analyse, understand and ultimately disclose climate-related

financial information. The wide international support for the TCFD recommendations across

large businesses, Governments, stock exchanges and the investment community has led the

government to adopt them as the basis for implementing climate-related financial disclosures

widely across the UK economy.

These regulations form part of concerted actions by the government and several regulators to

mandate TCFD-aligned climate-related financial disclosures. The government’s Net Zero

Strategy, published on 19

th

October 2021, highlights the importance of these disclosures to

inform investment decisions. More detail is provided in ‘Greening Finance: A Roadmap to

Sustainable Investing’, published on 18

th

October 2021

3

, which lays out the government’s

plans to build on these disclosure requirements to develop a wider strategy to give investors

and others the information they need to integrate climate change and sustainability in all

financial decisions.

3

‘Greening Finance: A Roadmap to Sustainable Investing’ is the Government’s document that sets out its long-

term ambition to green the financial system and align it with the UK’s net-zero commitment -

https://www.gov.uk/government/publications/greening-finance-a-roadmap-to-sustainable-investing

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

6

What are the requirements?

For companies:

The Companies (Strategic Report) (Climate-related Financial Disclosure) Regulations 2022

4

amend sections 414C, 414CA and 414CB of the Companies Act 2006 to place requirements

on certain publicly quoted companies and large private companies to incorporate TCFD-

aligned climate disclosures in their annual reports.

For LLPs:

The Limited Liability Partnerships (Climate-related Financial Disclosure) Regulations 2022

amend parts 5 and 5A of the Limited Liability Partnerships (Accounts and Audit) (Application of

Companies Act 2006) Regulations 2008

5

to place requirements on certain LLPs to incorporate

TCFD-aligned climate disclosures in their annual reporting.

For companies and LLPs:

Companies and LLPs within scope will be required to include disclosures on climate change-

related risks and opportunities, where these are material. The disclosures should cover how

climate change is addressed in corporate governance; the impacts on strategy; how climate-

related risks and opportunities are managed; and the performance measures and targets

applied in managing these issues.

This document provides answers to commonly asked questions to help companies within

scope to apply the Companies (Strategic Report) (Climate-related Financial Disclosure)

Regulations 2022; and to help LLPs within scope to apply the Limited Liability Partnerships

(Climate-related Financial Disclosure) Regulations 2022.

This document also sets out the outcomes desired in respect of each element of the disclosure

requirements common to the two sets of regulations. A non-exhaustive list of further guidance

produced by other bodies related to the TCFD recommendations is provided at the end of this

document.

The two sets of regulations will apply to the annual reports and accounts of companies and

LLPs within scope for accounting periods which start on or after 6

th

April 2022.

For companies:

Companies should include these disclosures in what was previously the Non-Financial

Information Statement, now the Non-Financial and Sustainability Information Statement in the

4

The Companies (Strategic Report) (Climate-related Financial Disclosure) Regulations 2022 -

https://www.legislation.gov.uk/uksi/2022/31/contents/made

5

The Limited Liability Partnerships (Accounts and Audit) (Application of Companies Act 2006) Regulations 2008 -

https://www.legislation.gov.uk/uksi/2008/1911/contents

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

7

Strategic Report. The Companies (Strategic Report) (Climate-related Financial Disclosure)

Regulations 2022 have introduced this change of name for this part of the Strategic Report.

The Companies (Strategic Report) (Climate-related Financial Disclosure) Regulations 2022

apply size thresholds to determine those companies which are required to comply with them.

The size thresholds are explained in this document. The size thresholds are intended to

engage the most significant companies in economic and environmental terms in analysing and

disclosing their climate-related risks and opportunities.

For LLPs:

LLPs should include their disclosures in either the Energy and Carbon Report of their Directors’

Report or, for those LLPs which prepare a Strategic Report, in that report.

The Limited Liability Partnerships (Climate-related Financial Disclosure) Regulations 2022

apply similar size thresholds to determine those LLPs required to comply with them.

C. Scope

The disclosure requirements will apply to your company or LLP if it meets the following scope

criteria:

All UK companies that are currently required to produce a non-financial information

statement, being UK companies that have more than 500 employees and have either

transferable securities admitted to trading on a UK regulated market or are banking

companies or insurance companies (Relevant Public Interest Entities (PIEs));

UK registered companies with securities admitted to AIM with more than 500 employees;

UK registered companies not included in the categories above, which have more than 500

employees and a turnover of more than £500m;

Large LLPs, which are not traded or banking LLPs, and have more than 500 employees and

a turnover of more than £500m and;

Traded or banking LLPs which have more than 500 employees.

Q1. Do the regulations apply equally across the UK?

The regulations apply in England, Wales and Scotland. They will also apply by agreement in

Northern Ireland.

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

8

Q2. Will disclosure be required at the group or subsidiary level?

Companies are expected to report at the group level (or at the company level if not included

within consolidated group reporting). Subsidiaries whose activities are included within a

consolidated group report of a UK parent that complies with the climate-related financial

disclosures requirements are not required to report separately.

Where a parent company does not produce consolidated accounts, the scope criteria should

be applied to the aggregated turnover and employee figures of the group headed by that

parent. In such situations, the climate-related financial disclosures should relate to the parent

company, including how climate-related risks and opportunities may affect the value of the

investment in those subsidiaries. A subsidiary of a parent company that does not produce

consolidated accounts, and that is within scope on an individual basis, should also make

climate-related financial disclosures in its individual accounts.

It is important that businesses consider their specific circumstances and relevant facts when

determining the appropriate disclosures. Where appropriate, legal advice should be taken.

Q3. Will UK companies be required to report on their global operations or just

their UK operations?

When a UK group is in scope the top UK parent is expected to report, within its Annual Report,

on the global operations of the UK group (regardless of whether activities are conducted

through a UK subsidiary or an overseas subsidiary).

Q4. Will UK companies with an overseas parent company be exempt?

There is an exemption from the disclosure requirements at company level where that

company’s activities are included in a consolidated report and there is a UK parent company.

Where a UK company has an overseas parent which reports on a consolidated basis, the

exemption does not apply.

Q5. What happens if a company or LLP within scope does not comply with the

disclosure requirements?

The Financial Reporting Council (FRC) has the responsibility to monitor the contents of

Strategic Reports and the power ultimately to make an application to the court for a declaration

that the annual report and accounts of a company do not comply, or a Strategic Report or a

Directors’ Report does not comply, with the requirements of the Companies Act. The court may

then order the preparation of revised accounts (including the revision of the strategic report)

and other such matters the court thinks fit.

The responsibilities of the company’s auditor still apply as with the rest of the Strategic Report.

Accordingly, in instances where the auditor has reviewed the climate disclosures and

determines these contain uncorrected material misstatements, this should then be recorded in

the auditor’s report.

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

9

D. Timing

Q1. When should companies and LLPs start complying with the new regulations?

Regulations will be in force on the Common Commencement Date of 6

th

April 2022 and will be

applicable for accounting periods starting on or after that date.

Q2. Will any companies or LLPs be exempt from complying on this date?

No. All companies and LLPs which fall within scope will need to comply with their respective

regulations.

E. Reporting requirements under sections 414CA and 414CB

of the Companies Act 2006 and Regulations 12A and 12B of

the Limited Liability Partnerships (Accounts and Audit)

(Application of Companies Act 2006) Regulations 2008.

Q1. What do the regulations require companies and LLPs to disclose?

These regulations for companies and LLPs both require climate-related financial disclosures to

be made against a common list of requirements. This guidance – see Question 3, below -

discusses the desired outcomes which companies should aim for in their disclosures against

each of these requirements.

Companies and LLPs are both required to disclose the following information:

(a) a description of the governance arrangements of the company or LLP in relation to

assessing and managing climate-related risks and opportunities;

(b) a description of how the company or LLP identifies, assesses, and manages climate-

related risks and opportunities;

(c) a description of how processes for identifying, assessing, and managing climate-related

risks are integrated into the overall risk management process in the company or LLP;

(d) a description of—

(i) the principal climate-related risks and opportunities arising in connection with the

operations of the company or LLP, and

(ii) the time periods by reference to which those risks and opportunities are assessed;

(e) a description of the actual and potential impacts of the principal climate-related risks and

opportunities on the business model and strategy of the company or LLP;

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

10

(f) an analysis of the resilience of the business model and strategy of the company or LLP,

taking into consideration of different climate-related scenarios;

(g) a description of the targets used by the company or LLPs to manage climate-related

risks and to realise climate-related opportunities and of performance against those targets; and

(h) the key performance indicators used to assess progress against targets used to

manage climate-related risks and realise climate-related opportunities and a description of the

calculations on which those key performance indicators are based.

Q2. Where should a company make its climate-related financial disclosures?

A relevant company should disclose its climate-related financial disclosures within the section

of the Non-Financial and Sustainability Information Statement. The regulations have introduced

this change of name.

Companies may also consider the FRC’s Guidance on the Strategic Report

6

, which

encourages companies to consider the importance of linking disclosures with other information

disclosed in an Annual Report. Linkages help readers to understand climate disclosures in a

broader context.

Q3. Where should LLPs disclose such information?

LLPs should include their disclosures in the Energy and Carbon Report or, if a Strategic Report

is prepared, within that report.

Q4. What information should companies and LLPs include on each element of

the reporting requirements?

The regulations require companies and LLPs to make the following disclosures, aligned with

the recommendations issued by the international Task Force on Climate-related Financial

Disclosures (TCFD). These disclosures are based on, but do not directly mirror the

recommendations from the Task Force. The TCFD’s recommendations have been adapted so

that they are suitable for inclusion in UK legislation.

a) a description of the company’s/LLP’s governance arrangements in relation to

assessing and managing climate-related risks and opportunities;

A company or LLP should disclose information which allows a user of its accounts to

understand how risks and opportunities relating to climate change are identified, considered,

and managed within its governance structure. The information should enable a user of the

accounts to understand which person or committee has the responsibility for identifying and

considering climate-related risks and opportunities, including how frequently those matters are

considered, and who has responsibility for managing those risks and opportunities. The

6

https://www.frc.org.uk/accountants/accounting-and-reporting-policy/clear-and-concise-and-wider-corporate-

reporting/narrative-reporting/guidance-on-the-strategic-report

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

11

information should also enable a user of the accounts to understand the extent to which

information relating to the climate-related risks and opportunities is considered by the Board.

If no directors have oversight of climate-related risks and opportunities and / or no person or

persons within the company have responsibility for assessing or managing climate-related

risks and opportunities, then this should be stated.

(b) a description of how the company or LLP identifies, assesses, and manages climate-

related risks and opportunities;

Companies and LLPs should disclose information that enables a user of the accounts to

understand the systems and processes in place that enable risks and opportunities associated

with climate change to be identified, assessed and managed. This should include information

to enable a user of the accounts to understand whether risks and opportunities are identified at

subsidiary level and reported up through the group or whether risk and opportunity

identification is done at group level only. It should also include how frequently this risk

identification exercise is required to be refreshed. This information will help users of the

accounts to assess the likely completeness of the disclosures relating to the company/LLP’s

exposure to climate change. The following requirements offer more detail on what should be

included in this description.

(c) a description of how processes for identifying, assessing, and managing climate-

related risks are integrated into the company’s/LLP’s overall risk management process;

Climate change is a systemic risk facing business; however, it is only one of a number of risks

that businesses must manage if they are to be successful. To understand properly the risks

and opportunities arising from climate change many businesses may have to undertake

separate exercises to ensure that those risks and opportunities are identified, understood and

properly taken into account in business decisions. Companies and LLPs may choose to

arrange training to help those responsible for managing risk to undertake these exercises; or to

hire additional expertise to perform this role. Over the longer term, however, it will be important

that businesses integrate the assessment of climate risk into overall risk management

processes and that climate risk is treated in the same way as the other risks that have the

potential to severely disrupt the company’s business model.

Companies or LLPs should provide disclosures which explain the extent to which climate-

related risk is currently integrated into the overall approach to risk management or whether the

identification, assessment and management of climate-related risks are subject to separate

processes and procedures. This information will help a reader of the accounts to understand

the maturity of the approach adopted in respect of climate-related risks, the level of resource

that has been assigned to understanding this systemic risk and whether process changes are

likely to occur in the future.

(d) a description of—

(i) the principal climate-related risks and opportunities arising in connection with the

company’s operations, and

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

12

(ii) the time periods by reference to which those risks and opportunities are assessed;

(e) a description of the actual and potential impacts of the principal climate-related risks

and opportunities on the company’s/LLP’s business model and strategy;

Guidance related to disclosures (d) and (e) is presented together, as impacts should be

considered in respect of each of the risks identified, together with mitigating actions. This

should provide a clearer narrative for the reader of the accounts.

Risks (d) (i) & (ii):

Climate-related risks and opportunities may arise in the short term, medium term, or over a

period of time which may be outside the company or LLP’s usual planning cycle. It is essential

that in identifying climate-related risks and opportunities a business should consider all

relevant time horizons, not just those that are usually considered for budgetary, strategy or

planning purposes.

The disclosure of the climate-related risks and opportunities should enable a user of the

accounts to understand the risk or opportunity posed by climate change and to understand the

potential effect of that risk or opportunity on the business. The disclosures should also enable

a user of the accounts to understand the mitigations, where appropriate, that a business has

already put in place and the mitigating actions that it is planning to take. It is also necessary to

provide information which enables a user of the accounts to understand the likely time periods

over which the risk or opportunity is expected to crystallise.

The risks and opportunities should be categorised, wherever possible, into short term, medium

term and long term and the company or LLP should explain how it has determined the time

periods that it is treating as short, medium and long term. The assessment of the appropriate

time periods for short, medium and long term should take into account the nature of the

company or LLP’s business and operations and may include factors such as the budgetary

cycle, asset lives, length of financing arrangements and the periods over which climate risks

and opportunities are expected to affect the business.

Where material to the business, it may be relevant to distinguish between “physical” climate

change risks, such as increased frequency of extreme weather events or sustained impacts

from temperature rises, for example, to supply and distribution arrangements, and “transition”

risks, that is, risks associated with transition to a net zero economy, which might prompt review

or adaptation of business models.

Physical risks:

Companies and LLPs should consider both acute physical risks (e.g., higher frequency or

severity of weather-related events such as winter storms, surge floods, hail and wildfires) and

chronic physical risks (e.g., longer-term changes to weather patterns and associated sea-level

rises, hot or cold waves and droughts). In determining the level of detail that is necessary to

meet this requirement, a company or LLP should consider the range of geographical locations

in which it operates, the extent to which those geographical locations may be subject to both

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

13

acute and chronic physical risks. Where elements of a supply chain or items of critical

infrastructure are likely to be exposed to increased physical risks, it may be important to

consider mitigating actions.

Transition risks:

Companies and LLPs should consider a range of transition risks and opportunities most

relevant to their products and markets. In identifying risks and opportunities, relevant climate

“transition” risks across the spectrum of technology, policy, market and legal and reputational,

associated with mitigation of and adaptation to climate change should be considered.

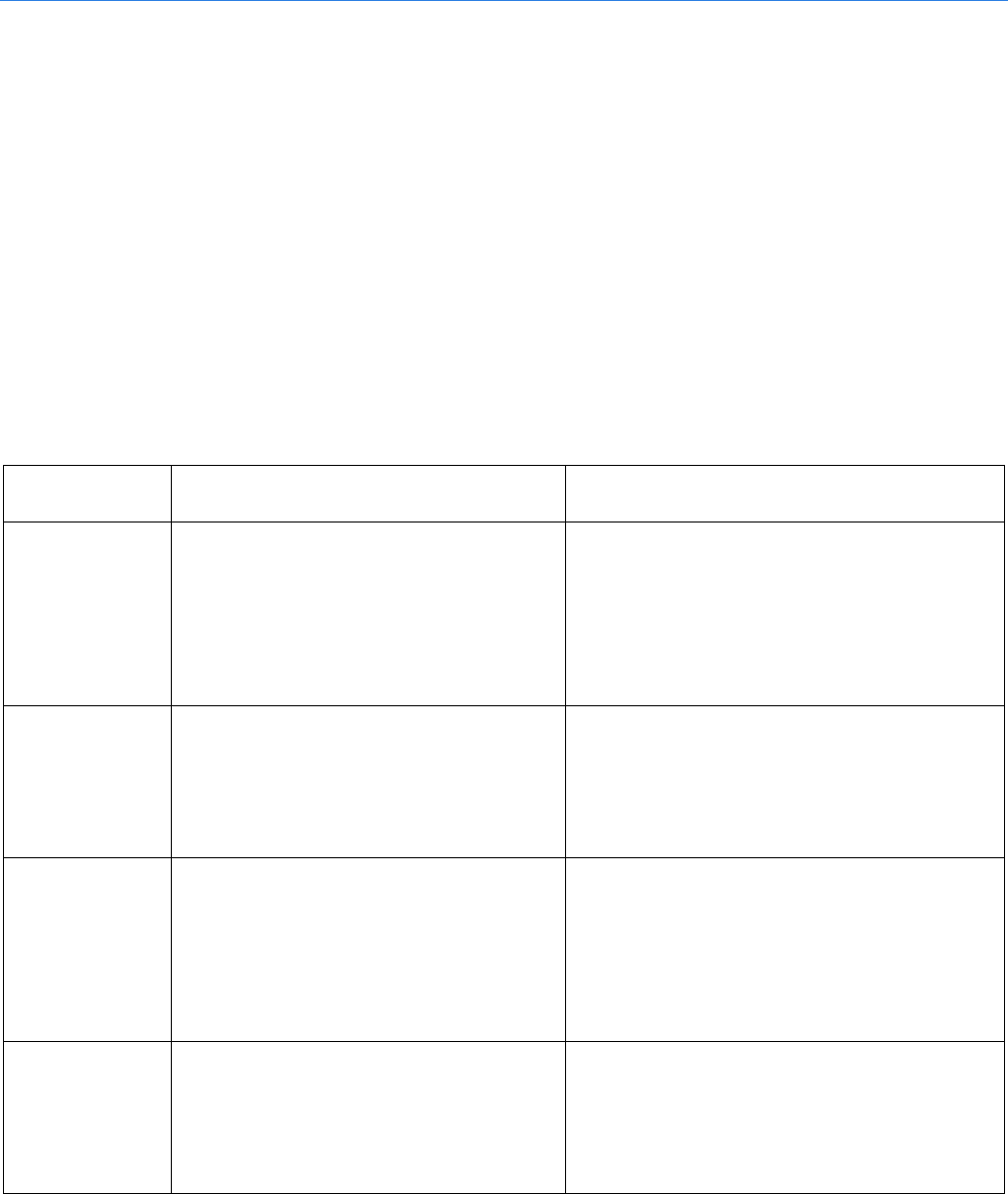

Companies and LLPs should consider which risks may have the greatest potential impact and

which risks may have the greatest likelihood of materialising. For instance, figure 1 below

provides examples of some transition risks and opportunities that may be relevant to some

companies and LLPs. This is an illustrative list and is not exhaustive.

Risk type Risk example Opportunity example

Technology A lower-carbon technology,

deemed to be a competitor to your

own, takes market share as

emissions-reductions solutions are

sought.

A lower-carbon technology, which may

be used as an input for your

processes, reduces in price due to

increased investment and use.

Policy A regulatory change may impact

the sale of your product or service

over a certain timeframe.

Government intervention may support

the cost-effectiveness of certain lower-

carbon technologies you use as an

input.

Market Consumer demand for higher-

carbon products you produce

reduces as spending power shifts

to more climate-conscious

consumers.

New markets and consumers are

attracted to a product or service you

provide as a result of a positive or

neutral climate impact.

Legal and

reputational

A climate-related incident affecting

an industry competitor increases

scrutiny of your operations and

environmental impacts.

A legal ruling applies more stringent

emissions reduction requirements on

an industry you supply, making your

lower-carbon product more attractive.

Figure 1 – non-exhaustive list of climate-related risks and opportunities.

Impacts (e):

The principal climate-related risks identified above are those which have the potential to have a

significant negative or positive impact on the company or LLP’s business model and/or

strategy. The description of the actual and potential impacts should be as granular as is

necessary to understand the impact of crystallisation of that risk and should be specific. In

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

14

describing the actual or potential impact a business should consider both the actions that are

being put in place now and contingency plans for actions which may be taken in the future.

For instance, when considering the impacts of physical risks, a manufacturer may have

identified that one of its major plants is situated in a location which is becoming more prone to

flooding as a result of climate change. The disclosures should enable a user of the accounts to

understand which plant or plants may be at physical risk, the importance of that plant to the

business and the impact that a major flood affecting that plant would have on the business

model and strategy. The description of the impact of a flood could include, for instance, the

importance of the production of that plant to the business as a whole, supply chain contingency

plans that the business may put in place to source parts from alternative sources, whether

flood defences are being improved or whether relocation is being considered and, if so, the

implications for the business of such a relocation.

For instance, when considering the impacts of technology or policy-related transition risks, a

company or LLP might face costs of transitioning to low emissions technologies, perhaps

resulting in retirements of existing assets, research and development of new solutions, capital

expenditure on new technologies or adoption of new processes or practices. Conversely, a

company or LLP might expect a reduction in costs over time as a lower-carbon energy source

becomes more cost-effective or resource efficiencies lead to a reduction in costs.

For instance, when considering the impacts of market-related transition risks, a company or

LLP might be exposed to shifting consumer preferences and spending power towards more

climate-conscious products and services, and a resulting reduction in demand. Conversely, a

company or LLP might set out where existing products and services are likely to attract new

demand, or where new products or services could be developed to attract demand from

climate-conscious consumers and markets.

For instance, when considering the impacts of legal or reputational-related transition risks, a

company of LLP might face direct costs of legal challenges, or costs associated with increased

scrutiny as a result of legal challenges made within relevant industries. Conversely, a company

or LLP might expect an increase in revenue or profitability for certain products or services as a

result of improved reputation stemming from positive climate-related actions.

Where such impacts are material to an understanding of the business or its strategy, they

should be disclosed.

(f) an analysis of the resilience of the company’s/LLP’s business model and strategy,

taking into account consideration of different climate-related scenarios;

The company or LLP should provide an assessment of the resilience of its business model and

strategy in the light of risks arising in the event of different climate change scenario projections.

Selecting scenarios:

The company or LLP should select scenarios which are most relevant to its business. These

scenarios could include a gradual required reduction in emissions or a sudden required

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

15

reduction in emissions. Scenarios may also include a 1.5 degree C scenario or a ‘business as

usual’ scenario where temperatures are likely to continue on their current trajectory to reach

over 2 degrees C (e.g., a 3.5 degree C scenario). Climate scenarios typically take account of

the assessments of the Intergovernmental Panel on Climate Change and the targets of the

Paris Climate Agreement to reflect a global average temperature increase within the range of

1.5 degrees C above pre-industrial levels, to and including 2 degrees C above pre-industrial

levels. Scenarios should be sufficiently varied to cover a range of future outcomes relevant to

the business. The most appropriate choice of scenarios to consider will depend on the nature

of the risks and opportunities to which the business is most exposed.

For instance, a business which generates substantial emissions may consider scenarios where

those emissions are required to be reduced under different time frames and the effect on the

business resulting from those required reduction in emissions or may consider the financial

cost associated with a higher carbon price over a range of time horizons. Similarly, a business

which has substantial exposure to physical risks may consider the impact of a range of

warming scenarios on both acute and chronic physical risks, and the resulting impact on

assets and the infrastructure of supply chains exposed to those risks.

Disclosures should enable a reader to understand which scenarios have been used, including,

where appropriate, the source of those scenarios, and the effect that operating within that

scenario would have on the resilience of the current business model and strategy. Disclosures

should also enable a user of the accounts to understand why a particular scenario has been

chosen, for instance where the use of a particular scenario has become the industry norm.

Where mitigating actions are being put in place, disclosures should allow a user of the

accounts to understand the extent of the mitigating measures and residual risks and effects of

climate change.

Disclosure of assumptions and estimates:

The government acknowledges and expects that assumptions and estimates may be needed

to complete scenario analysis. It is important that businesses disclose the assumptions and

estimates that underpin the scenario analysis exercise. This will help enable a reader to judge

whether those assumptions and estimates are reasonable and in line with similar companies or

LLPs. The government expects that the complexity and sophistication of the assumptions and

estimates will grow over time as companies and LLPs become more familiar with performing

scenario analysis. Where assumptions and estimates change year on year, the disclosures

should enable a user of the accounts to understand how and why they have changed. The

government recognises that, at the outset, when the use of climate scenarios in disclosures

may be new to some businesses, there may be significant divergence in methodology,

assumptions and estimates. It anticipates there will be natural convergence within industries as

good practice emerges. In these circumstances, where divergence then persists, it would be

important to explain why outlier assumptions and estimates remain appropriate.

Qualitative scenario analysis:

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

16

Scenario analysis should be at least qualitative in approach. Qualitative scenario analysis uses

narratives to explore implications of different possible climate impacts. At the most basic, this

uses the question “what if..?” to introduce climate-related risks for consideration. To meet the

requirements of these regulations it is not necessary to produce quantitative scenario analysis,

though some companies and LLPs may find it useful to do so to support their strategy and risk

management considerations.

Disclosing results:

Companies and LLPs should look to evaluate and disclose resilience of their business model

and strategy according to the scenarios used. This process offers an opportunity then to

identify options to strengthen business resilience to plausible climate-related risks and

opportunities.

When starting out, companies may decide to focus on the most relevant geographies or lines

of business initially, building to a full analysis of the organisation and its operations over time.

Across economies and societies, climate scenarios and the understanding of the physical and

transition risks of climate change continue to develop. Alongside this, businesses and markets

naturally change and evolve over time. It may not be necessary to undertake climate scenario

analysis for the disclosures by companies and LLPs every year, however new analysis should

be undertaken where there is a significant change in assumptions, for example, due to a

change in the business or developments in climate science and predictions. In any event, the

climate scenario analysis should normally be renewed at least every 3 years to ensure the user

of the accounts is provided with up to date and relevant information. Given the value scenario

analysis can provide in supporting companies and LLPs in their assessment of climate risks

and opportunities, organisations may choose to conduct this analysis on an annual basis.

In addition, by way of background, the TCFD published a Technical Supplement in 2017 on

The Use of Scenario Analysis in Disclosure of Climate-Related Risks and Opportunities, which

offers guidance on how to approach scenario analysis and the common assumptions

underlying the analysis.

(g) a description of the targets used by the company/LLP to manage climate-related

risks and to realise climate-related opportunities and of performance against those

targets; and

(h) the key performance indicators used to assess progress against targets used to

manage climate-related risks and realise climate-related opportunities and a description

of the calculations on which those key performance indicators are based.

Where a company or LLP has set targets to help assess its progress in managing climate-

related risks and opportunities, the target should be properly explained, including the relevance

of the targets to the future operations of the company or LLP. The disclosure should include a

timeframe over which the company or LLP intends to meet those targets and how it monitors

and assesses progress in meeting those targets. The targets should, where possible, be linked

to the risks and impacts identified under disclosures (d), (e) and (f). Targets may be linked to

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

17

both an overarching reduction in emissions, and a reduction in individual risks and their

impacts that have been identified.

The company or LLP should explain which climate-related key performance indicators (KPIs) it

uses to assess progress against the targets set out under (g) to manage climate risks and

opportunities, how these are calculated, and, if different from the targets set, how the KPIs

relate to targets.

Where a company or LLP changes a climate-related KPI used to manage its climate-related

risks and opportunities, the reason for the change should normally be disclosed together with

explanations of why the new KPI is more effective than the previous measurements.

Q5. What level of detail is required?

The Non-Financial and Sustainability Information Statement must contain the climate-related

financial disclosures to enable a reader to understand the effect of climate-related financial

risks and opportunities on the business.

Disclosures should enable the reader to understand the information presented without needing

to refer to other sources of information produced by the company. Disclosures should enable

the reader to understand how the climate-related financial disclosures relate to the other

information presented in the Annual Report and should not omit information which, if disclosed,

would influence the decisions of investors. It is expected that investors will use this information

to make buying and selling decisions but will also use the disclosures in stewardship activities.

The disclosures should contribute towards the understanding of the business.

The duty of disclosure on company directors includes discretion to omit some or all of certain

disclosure requirements ((e), (f), (g) and (h) of the regulations – please see the list in the

response to Question 1, above) - where these are not considered necessary for an

understanding of the business, but if information is omitted as a result of relying on this

exemption, directors must provide a clear and reasoned explanation of their belief as to why it

is appropriate to omit the information.

Q6. Can the new information required be disclosed elsewhere?

All information that is provided to meet the disclosure requirements of the regulations must be

included within the Annual Report and Accounts. It is not necessary for all of the required

information to be located within the Non-Financial and Sustainability Information Statement,

but if included elsewhere in the Annual Report and Accounts, the Non-Financial and

Sustainability Information Statement must include a specific cross reference to where it can be

found.

If a company chooses to provide information additional to that required for meeting the

disclosure requirements of the regulations, this may be disclosed outside the Annual Report

and Accounts and may also be signposted within the Annual Report and Accounts. Such

signposting should make clear that the information is for further information only.

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

18

Q7. Should the information be disclosed in a particular format or structure?

No. The regulations do not prescribe a format for these climate-related disclosures.

Q8. Can I rely on third party information to make these disclosures and what

happens if that information is subsequently found to be inaccurate?

Directors are responsible for the information disclosed in the Annual Report. In the context of

the climate-related financial disclosures a company or LLP may choose to make use of

information which is generated by a third party in order to help them assess the climate-related

risks, for example, by contracting with a data provider to support the assessment and

disclosure of physical risks for certain assets or infrastructure. The legal duty to make the

climate-related financial disclosures will, however, remain on the directors.

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

19

Section 2

A. Interaction with other regulation and frameworks

Q1. How do these regulations apply to companies that are also subject to the

Financial Conduct Authority’s Listing Rule on TCFD disclosures?

The Financial Conduct Authority (FCA), via listing rule LR 9.8.6R (8)

7

, requires a commercial

company with a UK premium listing to make disclosures against the TCFD recommendations

and recommended disclosures on a “comply or explain basis”. This rule applies for accounting

periods beginning on or after 1st January 2021. The FCA extended the application of these

requirements to issuers of standard listed shares and global depositary receipts representing

equity shares (excluding standard listed investment entities and shell companies) via listing

rule LR 14.3.27R. These rules came into force for accounting periods beginning on or after 1st

January 2022. The FCA also introduced new TCFD-aligned disclosure rules for asset

managers and certain asset owners, which came into force for the largest firms on 1 January

2022 and will apply to smaller firms one year later. The disclosures required under these rules

are directed at clients and are separate to the listing rules. The rules are located in the FCA’s

ESG Sourcebook.

The FCA listing rules mean that certain UK premium listed companies and standard listed

companies must include a statement in their annual financial report which sets out whether

they have made disclosures consistent with the TCFD’s framework. Where disclosures have

not been made, there must be an explanation of why, and a description of any steps they are

taking or plan to take to make consistent disclosures in future. In accompanying guidance to

the listing rules, the FCA clarifies its expectations on these issues.

The FCA has also published guidance on its supervisory approach in respect of the listing

rules (Primary Market Bulletin 36

8

and (draft) Primary Market Technical Note 802.1

9

), which

also sets out how the FCA and FRC will work together to oversee climate-related disclosures

of in-scope listed companies’ Annual Financial Reports.

UK companies with more than 500 employees that are within the scope of FCA rules will be

subject to both the regulations and the relevant FCA rules. Since both sets of requirements are

based on the TCFD’s recommendations and recommended disclosures, there is a high degree

of consistency in the requirements. The main difference between the requirements is that the

FCA’s listing rules and accompanying guidance directly reference the TCFD’s

recommendations, recommended disclosures and specified TCFD-published guidance

materials; these regulations by contrast comprise specified climate-related disclosure

7

https://www.handbook.fca.org.uk/handbook/LR/9/8.html

8

https://www.fca.org.uk/publications/newsletters/primary-market-bulletin-36

9

Technical Note 802.1

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

20

requirements that are aligned with the TCFD’s recommendations, but do not directly reference

these.

Where a UK-registered listed company is subject to both sets of requirements, disclosure in a

manner consistent with all of the TCFD recommendations and recommended disclosures for

the purposes of the FCA’s listing rule in its annual report is likely to involve use of similar

information to the disclosures required by these regulations; therefore, it is normally likely to

meet the requirements of these regulations.

Q2. How are these regulations linked to the requirements for occupational

pension schemes to take actions on climate risk?

The Occupational Pension Scheme (Climate Change Governance and Reporting) Regulations

2021

10

, places requirements on trustees of certain large pension schemes to report in line with

TCFD; as well as improving their governance and actions to identify, assess and manage

climate risk.

Those large pension schemes are likely to have significant investments in companies that are

within scope of these regulations. Disclosures provided by companies will inform the

disclosures of large pension schemes under the pensions legislation.

Q3. How do the requirements of the regulations for climate-related disclosures

relate to Streamlined Energy and Carbon Reporting?

Emissions reporting forms a core part of evidencing how climate risks and opportunities are

being managed over time. The principal regulatory regime for the disclosure of emissions in

the UK was set out in the Streamlined Energy and Carbon Report (SECR). These regulations

complement, and do not duplicate, existing SECR requirements for quoted companies to report

on their global energy use and for large businesses to report their UK annual energy use and

greenhouse gas emissions. For the relevant companies, the requirements are set out in the

Large and Medium-sized Companies and Groups (Accounts and Reports) Regulations 2008 SI

2008/410. For LLPs, the requirements are set out in the LLPs (Accounts & Audit) (Application

of Companies Act 2006) Regulations 2008 SI 2008/1911.

Q4. How do these regulations relate to accounting standards and financial

statements?

There should be consistency between the information disclosed in line with these regulations,

and the financial statements. Where climate-related risks and opportunities identified by a

company or LLP are material, the impact of those risks and opportunities on the financial

statements should be considered in accordance with relevant accounting standards.

Estimates, assumptions and judgments used in preparing the financial statements should be

consistent with the estimates, assumptions and judgments used in the climate-related financial

disclosures.

10

https://www.legislation.gov.uk/ukdsi/2021/9780348224382

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

21

Q5. How do these regulations interact with the development of International

Sustainability Disclosure Standards?

The government has strongly backed the creation of the International

Sustainability Standards Board (ISSB) by the International Financial Reporting

Standards (IFRS) Foundation. The ISSB is expected to issue disclosure standards on a range

of environmental, social and governance topics, with the first standard being on climate. The

climate standard is expected to be substantially based on the TCFD recommendations, and

therefore the disclosure obligations introduced by these regulations are expected to be largely

consistent with the international standard.

BEIS is working on measures which will allow the government to adopt these international

standards for use in the UK and to require certain companies to report against them.

The government published on 18

th

October 2021 “Greening Finance: A Roadmap to

Sustainable Investing”, its strategy for sustainability disclosures, which aims to give investors

and other market participants the information they need to make climate change and

sustainability factors in every financial decision. Requiring certain large companies to report

against the international standards adopted for use in the UK is a key part of the Sustainability

Disclosure Requirements Regime set out in the Roadmap.

International standards for sustainability reporting will help to achieve consistent and

comparable reporting by businesses on these matters in the years to come.

B. Links to additional information

The links to other guidance are provided for further information only. These links do not

constitute government guidance nor inform compliance with the new disclosure requirements

but may offer helpful resources for companies and LLPs who wish to understand climate-

related financial disclosure in further detail. This is not an exhaustive list; other examples may

be available.

It is important to note that some of the resources here set out further information related to

climate change disclosure which go beyond the requirements set out in these regulations.

• Recommendations of the Task Force on Climate-Related Financial Disclosures (2017).

The TCFD’s recommendations for a framework for climate-related disclosures by

businesses may be viewed at: https://www.fsb-tcfd.org/publications/#recommendations

• Task Force on Climate-Related Financial Disclosures publications. The TCFD makes

available its latest publications at: https://www.fsb-tcfd.org/publications/

• TCFD technical supplement on scenario analysis. The TCFD published a note on

approaching scenario analysis in 2017, which may be viewed at:

https://www.tcfdhub.org/resource/tcfd-recommendations-technical-supplement-the-use-

of-scenario-analysis-in-disclosure-of-climate-related-risks-and-opportunities/

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

22

• The Financial Conduct Authority’s climate-related listing rule. The FCA’s climate related

reporting requirements are set out at: https://www.fca.org.uk/firms/climate-change-

sustainable-finance/reporting-requirements

• The Occupational Pension Scheme (Climate Change Governance and Reporting)

Regulations 2021. https://www.gov.uk/government/consultations/taking-action-on-

climate-risk-improving-governance-and-reporting-by-occupational-pension-schemes-

response-and-consultation-on-regulations/the-occupational-pension-schemes-climate-

change-governance-and-reporting-regulations-2021

• Streamlined Energy and Carbon Reporting (SECR). Guidance on the (The Companies

(Directors’ Report) and Limited Liability Partnerships (Energy and Carbon Report)

Regulations 2018) is included in the Environmental Reporting Guidance:

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachmen

t_data/file/850130/Env-reporting-guidance_inc_SECR_31March.pdf

• Network for Greening the Financial System Scenarios Portal: this is an international

network of central banks and supervisors, including the Bank of England, which is

developing climate and environmental risk management in the financial industry,

including consideration of climate scenarios. See:www.ngfs.net/ngfs-scenarios-portal

• The International Sustainability Standards Board. The progress towards international

sustainability standards may be tracked via: https://www.ifrs.org/groups/international-

sustainability-standards-board/

Mandatory climate-related financial disclosures by publicly quoted companies, large private companies

and LLPs

23

This publication is available from: www.gov.uk/government/publications/climate-related-

financial-disclosures-for-companies-and-limited-liability-partnerships-llps

If you need a version of this document in a more accessible format, please email

enquiries@beis.gov.uk. Please tell us what format you need. It will help us if you say what

assistive technology you use.